How I Tackle Kindergarten Costs with Smart Investment Tools

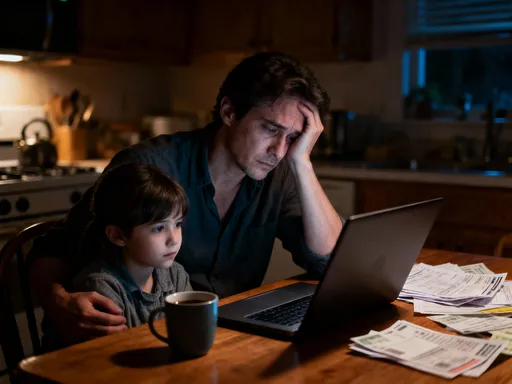

Paying for kindergarten shouldn’t mean draining your savings. I learned this the hard way—watching early education bills pile up while my budget slipped. But over time, I discovered practical investment tools that actually work. They’re not flashy or risky, just solid strategies focused on growth, safety, and long-term planning. In this article, I’ll walk you through how families can prepare financially, protect their funds, and make smarter moves without stress. The journey began with a simple realization: treating kindergarten as a short-term expense leads to long-term strain. By shifting to a proactive mindset, many parents find they can meet these costs without sacrificing peace of mind or future goals.

The Hidden Price of Early Education

When most parents think about kindergarten costs, tuition is the first number that comes to mind. However, the true financial footprint of early education extends far beyond monthly fees. A full assessment includes classroom supplies, field trips, transportation, school events, and even clothing appropriate for daily activities. In some communities, families also face additional charges for after-school care or enrichment programs such as music, art, or language classes. These expenses, while seemingly minor on their own, accumulate quickly. For example, a typical urban family might spend $150 per month on supplies and activities, adding up to nearly $1,800 over a single academic year. Over two or three years of preschool and kindergarten, that total exceeds $5,000—a sum that can strain even moderately tight budgets.

Beyond direct out-of-pocket costs, there’s another layer often overlooked: the opportunity cost for parents. When one caregiver reduces work hours or leaves employment to manage school drop-offs, pickups, or unexpected closures, household income takes a hit. For a parent earning $25 per hour, cutting back by just 10 hours a month means forgoing $3,000 annually. This invisible cost compounds the financial pressure, making early education not just an expense, but a structural shift in family economics. Treating it as a temporary burden rather than a planned milestone can lead to reactive decision-making—like relying on credit cards or delaying other essential savings goals.

What makes this challenge even more pressing is the timing. Kindergarten often arrives at a life stage when families are already managing mortgage payments, childcare for younger siblings, or student loan obligations. Without advance preparation, these overlapping demands can create a cash flow crunch. Yet many households wait until the enrollment period to assess affordability, by which time options are limited. The key insight is this: early education is not an isolated cost, but part of a broader financial journey. Recognizing its full scope allows families to shift from crisis management to strategic planning. Once parents see the complete picture, they become more motivated to explore tools that do more than just store money—they grow it.

Why Investment Tools Beat Savings Alone

It’s natural to think of a savings account as the safest place for money set aside for kindergarten. After all, the funds are accessible, insured, and free from market fluctuations. But safety comes at a cost—specifically, the cost of inflation. Over the past decade, the average annual inflation rate in the United States has hovered around 2% to 3%. Meanwhile, traditional savings accounts offer interest rates well below 1% for most consumers. This means that money sitting in a standard account loses purchasing power over time. A dollar saved today will buy less two or three years from now, even if the balance appears unchanged. For families saving for kindergarten, this erosion can silently undermine their efforts.

Investment tools, even conservative ones, offer a way to counteract this loss. Unlike passive saving, investing puts money to work, allowing it to grow through interest, dividends, or capital appreciation. Take, for instance, a parent who begins setting aside $100 per month two years before kindergarten starts. If kept in a savings account earning 0.5% interest, the total would be approximately $2,406 after 24 months. But if invested in a diversified, low-cost index fund averaging a modest 5% annual return, the same contributions could grow to about $2,500—an extra $94 without increasing the monthly commitment. That difference might cover textbooks, a laptop for learning, or even a portion of registration fees.

The real advantage lies in compound growth, which rewards consistency and time. Even small amounts, when invested early, benefit from earnings being reinvested and generating their own returns. This effect becomes more pronounced over longer periods, but even short-term horizons of two to five years can yield meaningful results. The key is understanding that investing for early education doesn’t require aggressive stock trading or high-risk bets. Conservative vehicles like bond funds, target-date funds, or education-specific accounts are designed to balance growth with stability. By embracing this approach, families move from merely preserving money to actively growing it, reducing the need to dip into emergency funds or delay other financial goals.

Another benefit of investing is psychological. When parents see their savings grow, they gain confidence in their ability to manage future expenses. This sense of progress reinforces disciplined habits, making it easier to stay committed. In contrast, watching a stagnant balance in a savings account can lead to discouragement or impulsive spending. Investment tools, therefore, serve a dual purpose: they enhance financial outcomes and strengthen financial behavior. The shift from saving to investing isn’t about chasing wealth—it’s about making money work smarter for a specific, meaningful goal.

Matching Goals with the Right Investment Vehicles

Not every investment tool fits every family, and choosing the right one depends on several factors: time horizon, risk tolerance, tax considerations, and long-term goals. For kindergarten planning, which typically spans two to five years, the focus should be on vehicles that balance growth potential with capital preservation. Among the most effective options are 529 plans, custodial accounts, index funds, and education-specific exchange-traded funds (ETFs). Each has distinct features, benefits, and limitations that make them suitable for different circumstances.

529 college savings plans, though named for higher education, can also be used for K–12 expenses, including private kindergarten, up to $10,000 per year tax-free at the federal level. These accounts offer tax-deferred growth and tax-free withdrawals when used for qualified education costs. Many states also provide tax deductions or credits for contributions, enhancing their appeal. The trade-off is limited flexibility—funds used for non-educational purposes are subject to taxes and a 10% penalty on earnings. For families certain about using the money for schooling, this restriction is a small price for significant tax advantages. Moreover, 529 plans often come with age-based investment options that automatically adjust from growth-oriented to conservative allocations as the child approaches school age.

Custodial accounts, such as UTMA (Uniform Transfers to Minors Act) or UGMA (Uniform Gifts to Minors Act) accounts, offer more flexibility. Parents can invest in stocks, bonds, or mutual funds, and the funds can be used for any expense that benefits the child, not just tuition. However, once the child reaches the age of majority (usually 18 or 21, depending on the state), they gain full control of the account. This lack of long-term parental control makes custodial accounts better suited for families comfortable with eventual transfer of ownership. Additionally, these accounts can impact financial aid eligibility later in life, a consideration for those planning beyond kindergarten.

Index funds and ETFs provide another accessible route. By tracking broad market benchmarks like the S&P 500, they offer instant diversification and low fees. For parents who prefer hands-on management, these tools allow precise control over investment choices. A balanced portfolio might include a mix of equity index funds for growth and bond funds for stability. Robo-advisors can automate this process, adjusting allocations based on the family’s timeline and risk profile. The main advantage is liquidity—unlike 529 plans, there are no restrictions on withdrawals. The downside is the absence of tax benefits unless held within a tax-advantaged account. For families seeking flexibility and moderate growth, index funds and ETFs represent a powerful middle ground.

Balancing Risk Without Losing Peace of Mind

One of the biggest concerns parents have about investing for kindergarten is risk. After all, the timeline is relatively short—often just a few years—and the thought of losing money close to enrollment can be paralyzing. This fear is valid, but it shouldn’t prevent families from exploring investment options altogether. With the right strategies, it’s possible to manage risk effectively while still achieving meaningful growth. The goal isn’t to eliminate risk entirely, but to control it in a way that aligns with the family’s comfort level and financial goals.

Dollar-cost averaging is one of the most effective techniques for reducing market risk. Instead of investing a lump sum all at once, families contribute fixed amounts at regular intervals—for example, $200 per month into a 529 plan or brokerage account. This approach smooths out the impact of market volatility because purchases occur at different price points. When prices are high, fewer shares are bought; when prices dip, more shares are acquired. Over time, this leads to a lower average cost per share. For parents wary of market timing, dollar-cost averaging removes the pressure to predict peaks and troughs, making investing feel more predictable and less emotional.

Asset allocation is another cornerstone of risk management. It involves dividing investments among different asset classes—such as stocks, bonds, and cash equivalents—based on the investor’s timeline and risk tolerance. For a child entering kindergarten in three years, a conservative allocation might be 40% in equities, 50% in bonds, and 10% in cash. As the enrollment date approaches, the portfolio can gradually shift toward safer assets to protect gains. This dynamic approach balances the need for growth in the early years with the need for stability as the goal nears. Automated target-date funds, available in many 529 plans, handle this transition automatically, making it ideal for busy parents.

Diversification further strengthens this strategy. By spreading investments across different sectors, industries, and geographies, families reduce their exposure to any single point of failure. For example, a portfolio that includes both U.S. and international stocks, along with government and corporate bonds, is less vulnerable to a downturn in one area. Emotional discipline plays a role too. Market fluctuations are normal, but reacting impulsively—by selling during a dip—can lock in losses. Educating oneself about market cycles and maintaining a long-term perspective helps prevent fear-based decisions. Ultimately, a well-structured plan doesn’t guarantee profits, but it does provide a framework for making thoughtful, resilient choices.

Turning Theory into Action: Simple Steps to Start

Understanding investment strategies is one thing; implementing them is where real progress happens. Many parents hesitate to begin because they feel overwhelmed by choices, lack confidence, or believe they don’t have enough money to make a difference. The truth is, getting started doesn’t require perfection or large sums. It requires clarity, consistency, and a few practical steps. The journey can begin in a single afternoon with minimal effort.

The first step is setting a clear goal. Determine the total estimated cost of kindergarten, including tuition, supplies, transportation, and any additional programs. Break this down into a monthly savings target. For example, if the total is $6,000 over three years, the family needs to save about $167 per month. This number provides focus and makes the abstract goal tangible. Next, choose an appropriate account. For education-specific savings, a 529 plan is often the best starting point due to its tax advantages and ease of use. Many states offer plans with low fees and automatic enrollment options. For greater flexibility, a taxable brokerage account with a robo-advisor can provide diversified, low-maintenance investing.

Once the account is open, set up automatic contributions. Linking a bank account to the investment platform ensures that money is transferred consistently, reducing the temptation to skip payments. Automation also removes the mental burden of remembering to invest each month. Even small amounts, like $50 or $75, can build momentum over time. Tracking progress is equally important. Most platforms offer dashboards that show account growth, contribution history, and projected balances. Reviewing these metrics quarterly helps maintain motivation and allows for adjustments if life circumstances change.

For families unsure where to begin, starting with a single action can break the inertia. It might be researching state 529 plans, opening a custodial account, or scheduling a consultation with a financial advisor. The goal isn’t to do everything at once, but to build confidence through small wins. Over time, these actions compound into a reliable system that supports both immediate and future education needs.

Avoiding Common Traps Families Fall Into

Even with good intentions, many families encounter setbacks in their financial planning. Some of the most common pitfalls are avoidable with awareness and discipline. One frequent mistake is chasing high returns without understanding the risks. Tempted by stories of rapid gains, some parents invest in individual stocks, speculative assets, or unproven platforms promising outsized rewards. While these may yield short-term wins, they often lead to significant losses, especially in volatile markets. For kindergarten funding, where capital preservation is critical, such risks are unnecessary. A better approach is to focus on consistent, moderate growth through diversified, low-cost funds.

Another trap is ignoring fees. Investment products often come with management fees, transaction costs, or hidden expenses that erode returns over time. A fund with a 1% annual fee may seem small, but over five years, it can consume a noticeable portion of gains. Families should prioritize low-expense-ratio funds, especially index funds and ETFs, which typically charge less than 0.20% per year. Comparing fees across platforms and reading the fine print can save hundreds or even thousands of dollars in the long run.

A third common error is dipping into education funds for emergencies. While it’s tempting to use dedicated savings for unexpected car repairs, medical bills, or home repairs, doing so undermines the original goal. Once money is spent, it’s difficult to rebuild the balance, especially if contributions pause. The solution is to maintain a separate emergency fund for unforeseen expenses. Even a small buffer of $1,000 to $2,000 can prevent the need to raid education accounts. By keeping goals distinct, families protect their progress and maintain financial clarity.

Finally, procrastination remains a silent obstacle. Many parents delay starting because they feel they don’t have enough money or knowledge. But waiting reduces the power of compound growth and increases future pressure. Starting with even $25 per month is better than waiting for the “perfect” moment. Every dollar invested early has more time to grow. Discipline, not size, determines long-term success.

Building a Foundation That Lasts Beyond Kindergarten

The financial habits formed while preparing for kindergarten can have lasting benefits that extend far beyond the early school years. The discipline of setting goals, choosing appropriate tools, and staying consistent creates a framework for managing future education costs—from elementary school supplies to high school activities and eventually college tuition. Families who start early often find that the process becomes routine, reducing stress and increasing confidence with each passing year.

Moreover, these practices foster financial literacy not just for parents, but for children as well. When kids see their parents planning, saving, and investing, they absorb valuable lessons about responsibility, delayed gratification, and long-term thinking. Some families even involve older children in tracking progress or discussing goals, turning finance into a shared family value. This early exposure can shape healthier money habits that last a lifetime.

Ultimately, preparing for kindergarten isn’t just about covering a bill—it’s about building resilience. It’s about making intentional choices today that create stability tomorrow. The tools and strategies discussed here aren’t reserved for the wealthy or financially savvy; they are accessible to any family willing to take the first step. By treating early education as a planned milestone rather than a surprise expense, parents do more than ease financial pressure—they model foresight, care, and commitment. And in doing so, they give their children not just a strong academic start, but a foundation of security that supports every future dream.